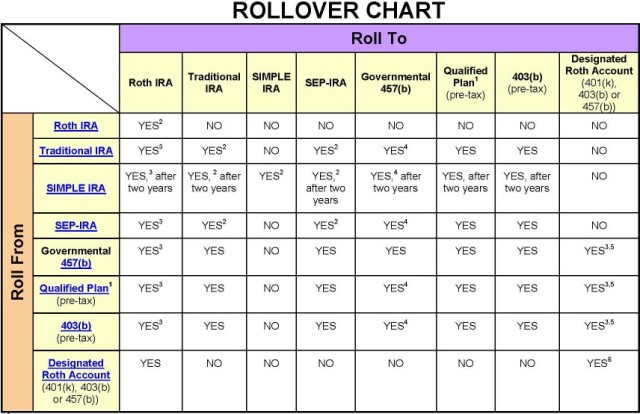

What’s an eligible rollover distribution and what’s not can be a complicated and confusing matter. Here’s a recent and handy rollover chart by the Internal Revenue Service updated for new rules that may be helpful.

1 Qualified plans include, for example, profit-sharing, 401(k), money purchase and defined benefit plans

2 Beginning in 2015, only one rollover in any 12-month period. A transitional rule may apply in 2015.

3 Must include in income

4 Must have separate accounts

5 Must be an in-plan rollover

6 Any amounts distributed must be rolled over via direct (trustee-to-trustee) transfer to be excludable from income

For more information regarding retirement plans and rollovers, visit Tax Information for Retirement Plans.

Editor’s Note: Hat tip to BenefitsLink.